Are The Sanctions Stopping Putin?

Plus: Christopher Rufo's Troll

Happy Thursday.

This is good: “U.S. Says It Secretly Removed Malware Worldwide, Pre-empting Russian Cyberattacks.”

The Biden administration has blocked Russia from using U.S. banks to make good on foreign debt payments, officials said, pitching Moscow closer to its first sovereign default in more than two decades.

The U.S. Treasury had previously granted special exemptions allowing the Kremlin to tap accounts at U.S. banks to repay its debts after banning such transactions as part of Washington’s sanctions campaign against Russia.

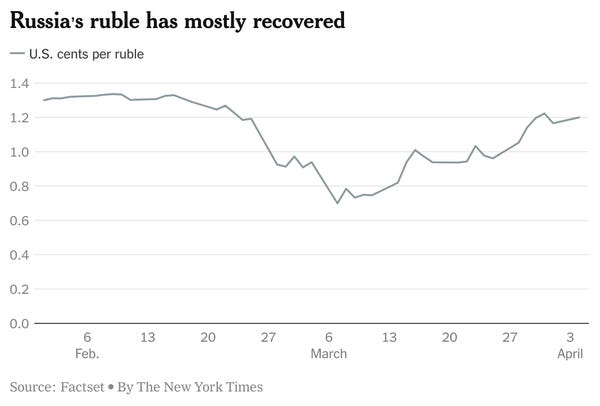

But I have questions. Two things caught my attention over the last 48 hours; the first is this: The Ruble is back.

What’s happening here? Via the NYT:

One reason currency experts were bearish on the ruble early in the war was that Russia’s reserves of foreign currencies held outside the country had been frozen. Ordinarily, Russia would spend those reserves to buy up rubles when the ruble was weak. With those reserves no longer accessible, it appeared that its central bank had become toothless.

But Russia doesn’t urgently need access to its foreign-exchange reserves because for now, at least, it has no shortage of dollars, euros and other foreign currencies.

But wait. We have been told over and over that the sanctions are “crushing,” and “crippling.” and would devastate the Russian economy and shake Putin’s uneasy throne. But, now we learn that Russia still has plenty of cash.

One major reason: The world — including our European allies, continue to buy massive amounts of Russian oil and gas, which is providing the Kremlin with the cash to help pay for its invasion of Ukraine.

This is the second thing that brought me up short: (Via Reuters):

Russia expects to earn 798.4 billion rubles ($9.6 billion) in additional revenue from energy sales in April due to high oil prices, the finance ministry said, as Moscow needs cash to finance its obligations while being cut off from its reserves.

It actually gets worse. (Via the NYT):

On April 1, economists for Bloomberg predicted Russia’s energy export earnings would increase by more than a third in 2022.

And while more hard currency is flowing in, less is flowing out. Western nations are punishing Russia for its invasion of Ukraine by cutting off sales of many products, both consumer and industrial goods. And Russian authorities are clamping down on imports that would use up foreign exchange.

The upshot is that Russia’s current account — the broadest measure of trade in goods and services plus investment income — is headed for a record surplus this year, according to the Institute of International Finance.

So, this seems suboptimal.

On our podcast the other day, the Wapo’s Josh Rogin talked about our inordinate faith in sanctions: “We tell ourselves stories about sanctions because Washington is addicted to sanctions; that’s the muscle memory of this town… So we can all pat ourselves on the back and believe we did what we could.”

To be sure, there are some signs that the sanctions are exacting a toll. CBS News, for example, reports that many educated Russians are fleeing the country and “Russia's economy is facing a contraction unlike any it's ever seen before.” CBS quotes a report from the Institute of International Finance that predicts that ‘The current crisis will wipe out 15 years of economic development.”

Which would be good.

But even as the war reaches a critical phase, there are growing questions about both the effectiveness of those sanctions in the short-term, and the proportionality of sanctions to respond to atrocities. Via the Wapo:

“The measures taken today by the U.S. and E.U. represent a significant tightening of an already tough set of measures. … However, given the nature of the atrocities being committed in Ukraine, it is fair to ask if these measures go far enough,” said Daniel Glaser, who served in the Treasury Department’s Office of Terrorism and Financial Intelligence under the Obama administration…“Oil and gas remain untouched and Russia continues to have access to the international financial system.”

This may change, but it’s worth asking, why has it taken so long? And, while we’re at it, perhaps we ought to also rethink our faith in the effectiveness of sanctions to deter the world’s monsters.

Christopher Rufo’s Troll

ICYMI, last weekend I got an email from outrage merchant Christopher Rufo’s new staffer.

Rufo, the charlatan who brought you the CRT panic, had been caught rather flagrantly misrepresenting a comment by a Disney executive.

Declaring that he had a “SCOOP”, Rufo had posted a video of Disney corporate president Karey Burke in which he claimed she said that she “wants a minimum of 50 percent of characters to be LGBTQIA and racial minorities.”

But, as I wrote, “The video doesn’t say that at all. Nowhere in the video posted by Rufo does Burke say that she “wants a minimum of 50 percent of characters to be LGBTQIA and racial minorities.”

Of course, everyone makes mistakes, and Rufo could have simply acknowledged his blunder, but instead he dispatched his “coalitions manager,” Armen Tooloee to demand a correction from me because mumblemumblemumble …someone else wrote something different someplace else or something. (You can read the whole thing here.)

It was a delicious many-layered onion of disingenuousness, so I responded to Tooloee’s email with one word: Nuts.

But the exchange prompted curious minds to ask: who is this Tooloee fellow? And why has Rufo hired him to push his latest crusade against “gayness” in Disney and the schools?